Celebrated internet analyst Mary Meeker has just released her 2019 Internet Trends report: one of the most highly-anticipated annual reports into the state of all things digital.

This year’s report is the first that Meeker has put out since leaving venture capital firm Kleiner Perkins to found her own late-stage VC firm, Bond Capital. Clocking in at a hefty 334 slides, it’s the second-longest Internet Trends report that Meeker has produced (the longest being 2017’s 355-slide tour de force) and a full 40 slides longer than her 2018 report.

As ever, the report is packed with fascinating statistics, trends and observations about the rapidly-changing world that we inhabit. Of particular interest are Meeker’s observations about the shifts in retail and ecommerce that are taking place on a global scale.

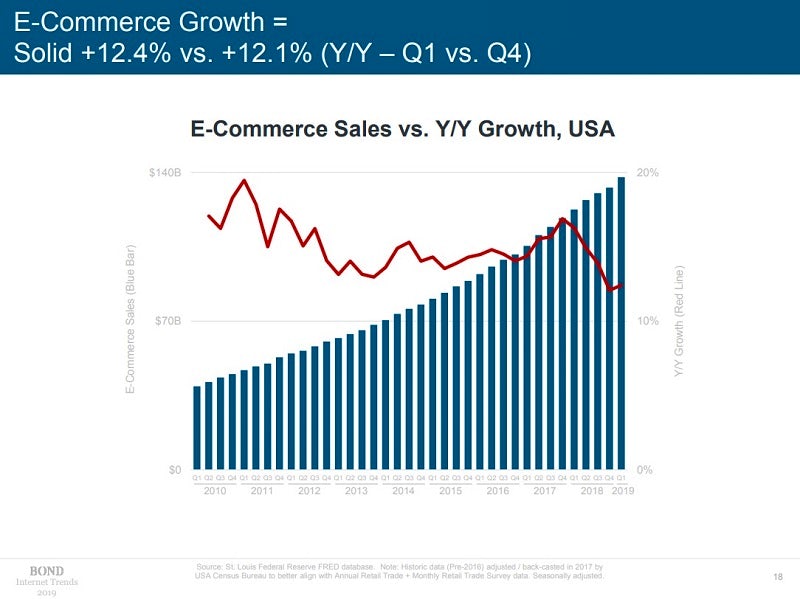

In the report’s second section, on Ecommerce and Advertising, Meeker notes that ecommerce sales growth in the USA is “solid”, reaching 12.4% year-over-year growth in Q1 of 2019, up from 12.1% in Q4 2018. Physical retail sales are also “solid”, albeit growing much more slowly at 2%, and ecommerce continues to make gains as a share of retail, reaching 15% of retail sales going into 2019.

But what’s most interesting about the growth of ecommerce in 2019 is that it isn’t just coming from the expected places – offline sales shifting to online, or customers visiting retailers’ websites to make purchases. Instead, Meeker’s Internet Trends report tells a story of shoppability becoming integrated into apps and services of every kind, offline retail becoming digitised, and ecommerce reaching new communities and demographics.

Here are the most noteworthy trends in ecommerce and retail from Mary Meeker’s Internet Trends 2019 report.

Messaging and social apps are increasingly becoming shoppable

In last year’s round-up of ecommerce trends from Meeker’s report, I noted that we seemed to finally be “getting somewhere” with social commerce, with users – particularly younger users – increasingly reporting product discovery and even purchases through social networks, and social networks referring an increasing share of users to ecommerce sites.

Since then, social commerce has become a reality almost overnight. After years of build-up, failed buy buttons and hybrid platforms that floundered, social commerce has arrived in the form of Instagram Checkout, an ecommerce checkout feature that allows users to shop directly from the many brands that promote their wares on Instagram.

Prior to the introduction of Checkout, brands – particularly fashion and beauty brands – were already driving plenty of sales through Instagram, but the new feature has allowed them to achieve this much more directly, and smoothed the buying experience on the user end as well.

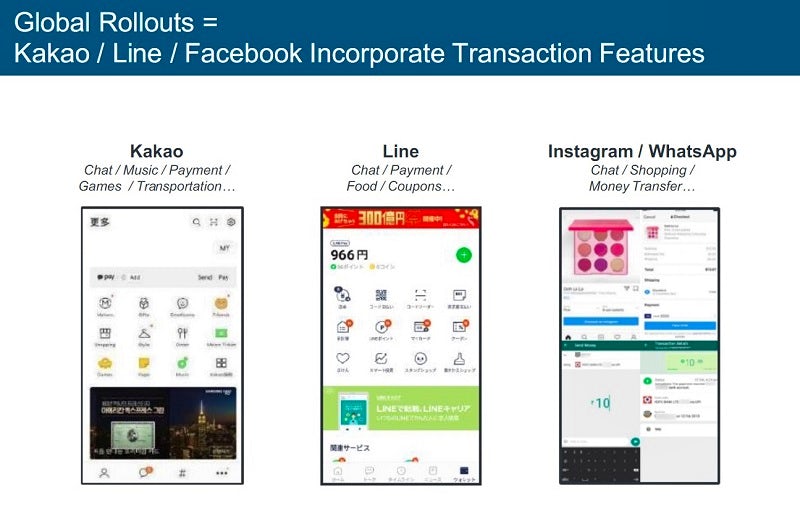

Meeker’s Internet Trends report situates this development within the wider context of social and messaging apps increasingly integrating ecommerce and transactional features. Meeker lists South Korean messaging app KakaoTalk, which integrated a mobile payments and digital wallet service, Kakao Pay, in 2014 as one example of this trend. Another example is Japanese messaging app Line, whose payments service, Line Pay, was also launched in 2014. Line has poured significant investment into Line Pay in recent months, injecting $182 million into its mobile payment business, and launching a partnership with Visa that will allow Line users to make use of Line Pay via a virtual visa card – even in places that the service isn’t supported.

Not content with making Instagram shoppable, Facebook has also slowly been introducing payment functionality to WhatsApp. The company first began trialling WhatsApp Pay in India in May 2018, and is now gearing up to roll the feature out in Europe, with London set to be a focal point of WhatsApp’s payments push.

WhatsApp Pay will give customers new ways to pay businesses when they make a purchase, but that’s not all. At Facebook’s recent F8 developer conference, Mark Zuckerberg announced a major new feature that will be coming to WhatsApp Business: Product Catalogs, a new way for businesses to display their product offerings directly within the app. While Zuckerberg didn’t spell out exactly how this will work, it isn’t a huge stretch to imagine it working in tandem with WhatsApp Pay to allow businesses to sell goods through WhatsApp.

Integrating ecommerce and payment functionality with social and messaging apps makes a great deal of sense given the immense amount of time that users spend in these apps, connecting with each other and with brands. It’s like setting up market stalls in an already crowded town square: why wouldn’t you go to where people already are, and allow them to shop seamlessly in the place where they socialise? Chinese super-app WeChat has already proven that this can be done, making a huge success of payments after it introduced WeChat Pay in 2015, and allowing ecommerce companies to set up mini-programs within its app that allow them to conveniently sell to its vast userbase.

Ecommerce platforms are stepping up their delivery

With consumers finding new ways to shop online in various different forms, the demand for fast, convenient delivery has risen rapidly. Increasingly, the speed and quality of a delivery can be a differentiator for ecommerce companies in a crowded marketplace: Amazon is famous for having built its empire around fast, guaranteed delivery with Prime, and in the process, has raised the bar for what consumers expect from an ecommerce company when it comes to delivery.

Meeker’s report highlights several companies around the world that have made delivery a focal point of their offering, and managed to cater to untapped or underserved communities by expanding their delivery network.

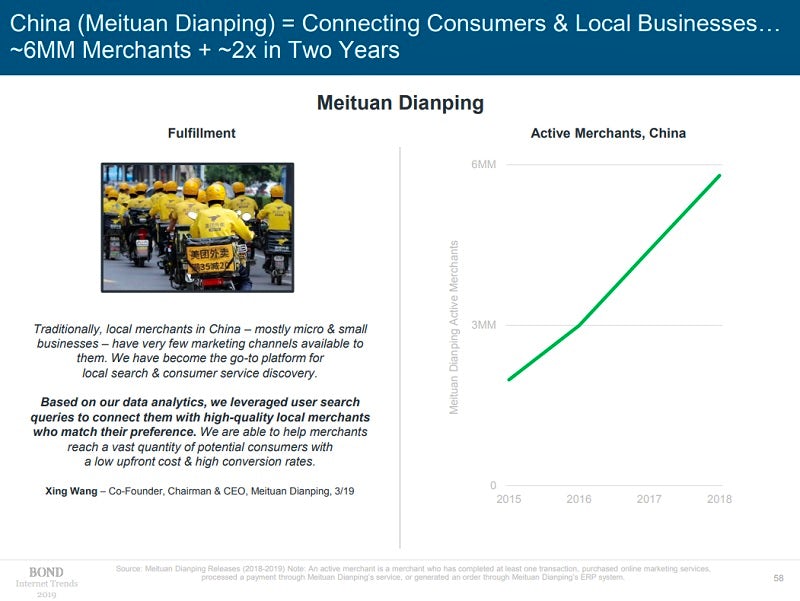

Meituan Dianping, a Chinese company that started out as a group buying platform and now offers everything from film tickets to home rentals, has succeeded in connecting an array of local merchants with consumers by using data analytics to match user search queries with high-quality local sellers. It has positioned itself as a combined marketing and fulfilment service, becoming the “go-to platform for local search and consumer service discovery” and “help[ing] merchants reach a vast quantity of potential consumers with a low up-front cost and high conversion rates”, in the words of its co-founder and CEO, Xing Wang.

In two years, Meituan Dianping has almost doubled its number of active merchants, going from three million active merchants in 2016 to nearly 6 million active merchants in 2018.

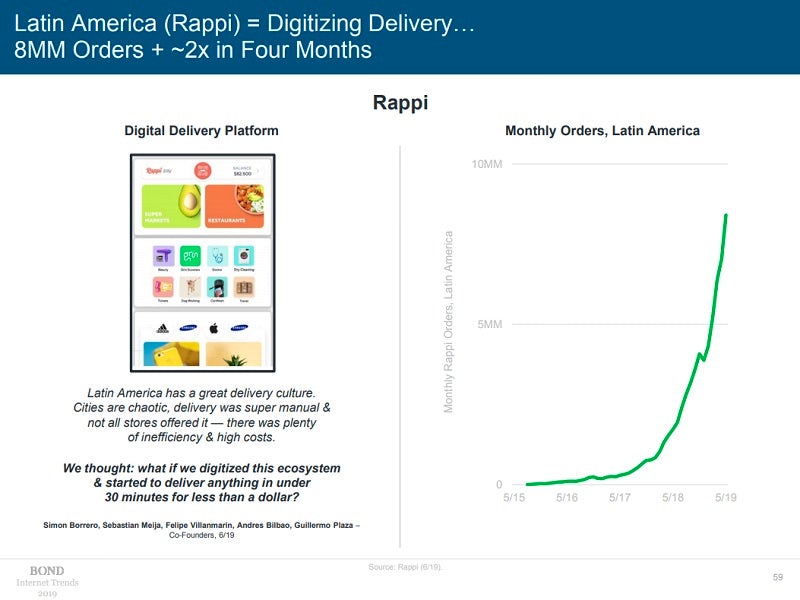

In Latin America, delivery start-up Rappi has found success in a competitive industry by “digitising” the delivery ecosystem of the countries that it serves – currently Argentina, Brazil, Chile, Colombia, Mexico, Peru and Uruguay. Meeker quotes Rappi’s co-founders as saying that while Latin America has a “great delivery culture”, there was “plenty of inefficiency and high costs” when they entered the market, with a lot of “manual” delivery and inconsistencies between retailers. So, the founders took it upon themselves to deliver “anything in under 30 minutes for less than a dollar”.

Much like other companies including Amazon and Uber who have disrupted markets by prioritising speed and cheapness of delivery, Rappi’s rise has had a human cost: in 2018, many of its workers went on strike to protest low pay and unsafe working conditions. However, its business success is hard to dispute, with monthly orders skyrocketing between May 2018 and May 2019, almost doubling over the course of four months in 2019, to reach a total of 8 million monthly orders across seven countries.

According to ZDNet, Rappi is now building out its offering into a technology platform for all kinds of products and services, from grocery and meal delivery to hiring scooters.

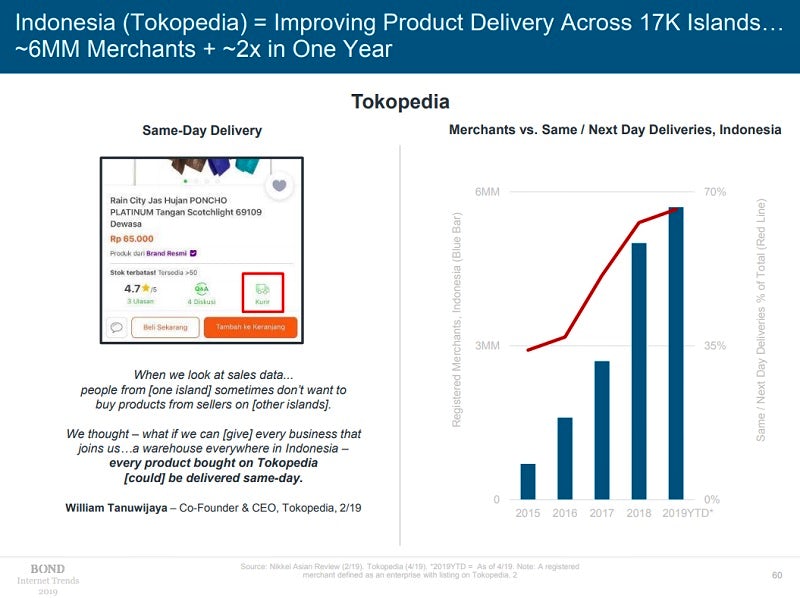

Another company that has opened up delivery in its target market is Tokopedia, an Indonesian ecommerce company. Its most well-known product is The Marketplace, a C2C platform that allows individuals and small businesses to set up online storefronts. Its founder, William Tanuwijaya, set out to connect merchants across Indonesia’s 17,000 islands who might have been missing out on demand from other parts of the country due to prohibitive shipping costs.

Tanuwijaya has created a network of warehouses across the islands through partnerships with logistics companies and warehouse operators, and used AI (building off a decade’s worth of sales data) to predict where inventory needs to be placed to get to prospective customers faster. Tokopedia has also kept costs low for marketers who want to start selling on its platform, by allowing them to list on the site for free, and not taking a cut of their sales. However, it might charge a fee for a merchant in one part of Indonesia to secure warehouse space in another.

As a result, the number of merchants on Tokopedia’s platform has nearly quadrupled between 2016 and 2019, growing from around 1.5 million in 2016 to close to 6 billion as of April 2019. Over the same time period, the percentage of deliveries that Tokopedia has fulfilled on the same or next day has grown from 35% to close to 70%.

As Meeker points out at the beginning of the section, data-driven and direct fulfilment is growing rapidly, allowing local merchants to expand their businesses by selling online, and bringing ecommerce to customers in new markets at affordable prices with fast delivery.

China: innovating grocery retail

As has been the case for the past few years, Meeker’s 2019 report contains a dedicated section on trends in China, provided by Hillhouse Capital – although there are also numerous statistics and case studies from China to be found throughout the rest of the report.

This year, Meeker has zeroed in on the way that China’s grocery retailers are innovating how they sell to consumers. She divides retailers into four categories depending on the level of service they offer.

The first category consists of Alibaba’s Freshippo (formerly known as Hema) and JD.com’s 7Fresh, both known as the pioneers of China’s offline-online ‘new retail’ model. Both retailers own and operate offline stores (more than 135 in the case of Freshippo) that allow consumers to order items for pick-up or delivery via an app, with all payment carried out digitally.

The second category includes online-only grocery stores Miss Fresh, Dingdong Maicai and Pupu Shengxian, which exhibit fresh goods within their app and deliver them within 30 minutes from a nearby warehouse. Each of these companies has owned-and-operated inventory and fulfilment, but no physical stores.

The third category encompasses retailers that allow customers to order through an app or group buy using WeChat mini-programs for next-day delivery or pickup, including Xingsheng Youxuan, Songshu Pinpin and Dailuobo. Unlike retailers in the second category, these retailers don’t own and operate inventory and fulfilment, but work with franchised community partners to deliver goods.

The fourth category of grocery retailers combines characteristics from the second and third categories, allowing customers to order in an app and using partner stores to fulfil the order. The retailers – which include Meituan, a multi-service super-platform, Ele.me, Taoxianda and JD Daojia – own the delivery process, and all offer delivery within 30 minutes.

In a single slide, Meeker showcases the sheer variety of grocery retailers competing to offer fresh goods to Chinese consumers, and the variety of ways that they are delivering them – methods that may well catch on in other markets with similar infrastructure.

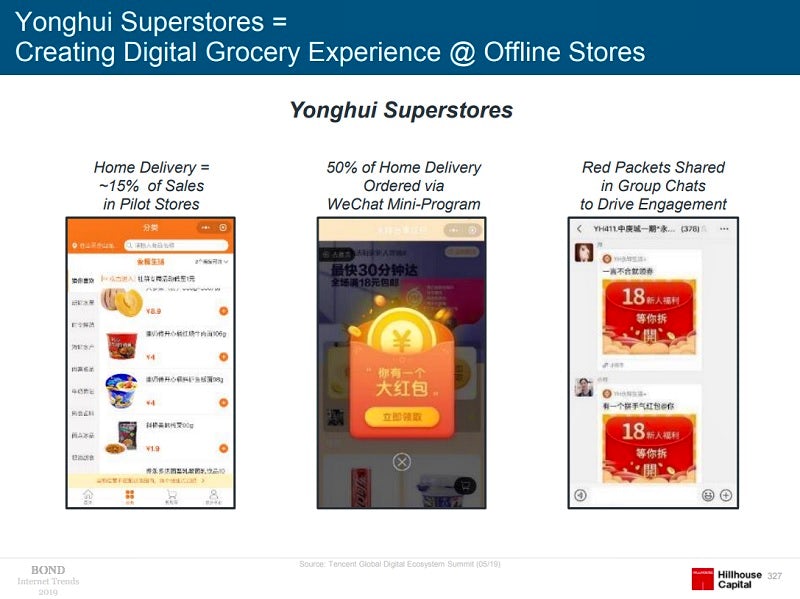

Meeker also shines a spotlight onto Yonghui Superstores, a department store chain backed by tech giant Tencent that has created a “digital grocery experience” in offline stores.

Yonghui has succeeded in bucking the trend of struggling brick-and-mortar retailers, particularly department stores, in China, 150 of which closed between 2012 and 2016. In 2017, Yonghui launched a range of smaller supermarkets (in comparison to its usual vast, hypermarket-sized stores) called ‘Super Species’ stores, aimed at introducing middle-class consumers to its online platform.

Other niche store concepts launched by Yonghui have included ‘YH Member Experience’ and ‘YH Life’, both offering online sales to customers living in the nearby area, with the added convenience of delivery. Meeker highlights that home delivery makes up roughly 15% of sales in Yonghui’s pilot stores, with 50% of home delivery ordered through Yonghui’s WeChat mini-program.

At a time when brick-and-mortar retailers across the world are struggling to stay afloat, retail brands could potentially take a leaf or two out of Yonghui’s book when it comes to combine digital convenience with offline retail.